7 Complete Pressure Washing Business Insurance Cost Factors for Contractors (2026)

22 min read·Updated April 4, 2026The average pressure washing business insurance cost ranges from $850 to $2,500 per year for a standard general liability policy with $1 million in coverage. Most owner-operators pay approximately $75 to $150 per month depending on their claims history, service area, and specific equipment used. Protecting your business requires more than just a basic policy; you must account for specialized risks like chemical runoff and surface damage. This guide provides exact 2026 pricing benchmarks and coverage requirements to ensure your exterior cleaning company remains profitable and protected.

Table of Contents

how to pressure washing business insurance cost: what you need and what it costs

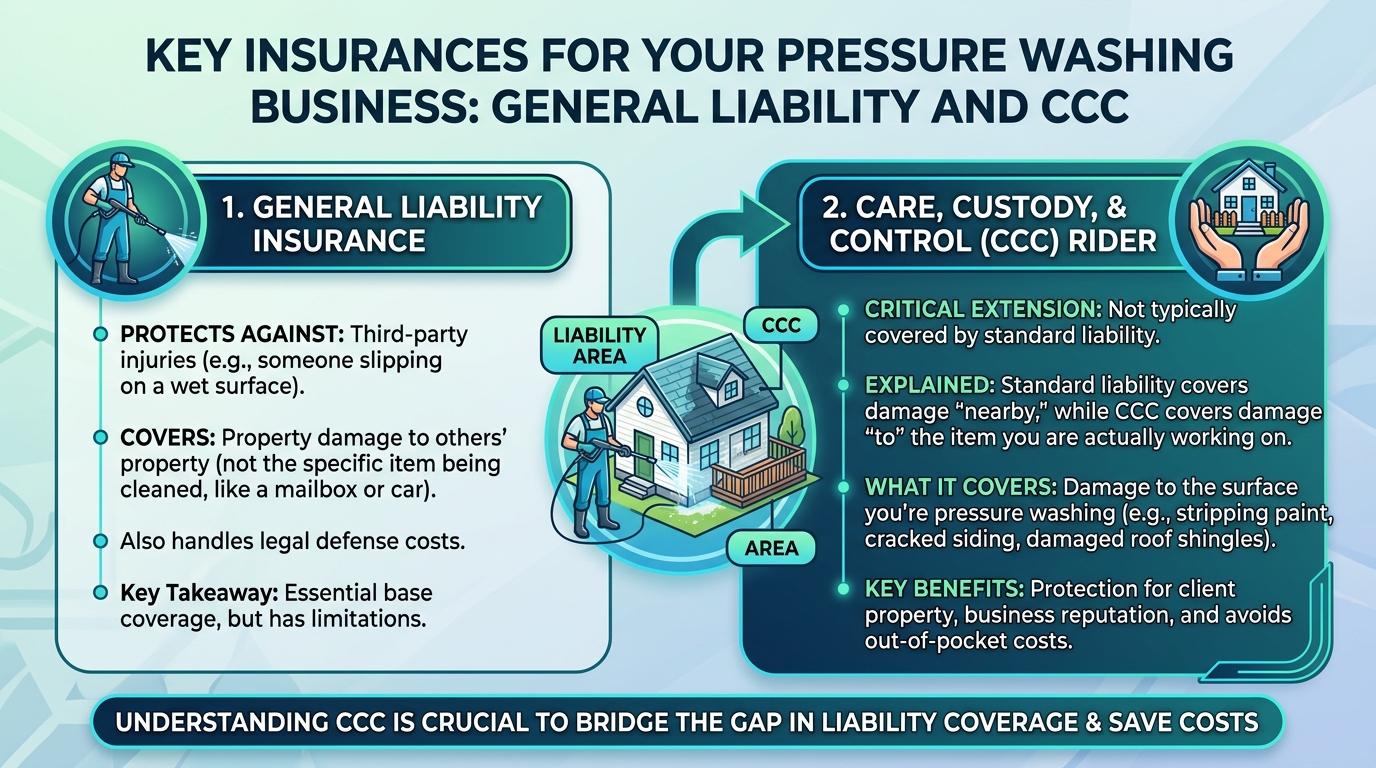

General Liability Insurance for Pressure Washers

General liability is the foundation of your protection, covering third-party bodily injury and property damage claims that occur during your operations. For a solo operator in 2026, a $1,000,000 per occurrence and $2,000,000 aggregate policy typically costs between $70 and $110 per month. This coverage is essential when you consider that a single high-pressure mistake can shatter a $1,200 custom window or cause a slip-and-fall accident on a wet driveway. Most commercial clients will require you to provide a Certificate of Insurance (COI) reflecting these minimum limits before you can even step onto their property.

The cost of general liability is heavily influenced by your annual gross revenue and the specific services you offer, such as roof cleaning or high-rise work. If your business scales to $250,000 in annual revenue, you can expect your premium to increase to roughly $1,800 to $2,400 per year. Insurance carriers like Hiscox and Next Insurance use these revenue benchmarks to calculate the likelihood of a claim occurring over a 12-month period. Adding 'Care, Custody, and Control' (CCC) endorsements is a critical step that many beginners overlook, as standard policies often exclude damage to the property you are actually cleaning.

You should also consider the impact of your service location on these initial premium quotes. Contractors operating in high-litigation states like Florida or California may see premiums that are 20% to 30% higher than those in rural areas of the Midwest. For example, a pressure washer in Miami might pay $1,500 for the same coverage that a contractor in Des Moines secures for $900. Always ensure your policy includes completed operations coverage, which protects you if a leak or damage is discovered weeks after you have finished the job and left the site.

Understanding Care, Custody, and Control (CCC) Riders

Standard general liability policies often contain an exclusion for damage to property that is in your 'care, custody, or control.' In the pressure washing industry, this means if you strip the finish off an expensive mahogany deck, a basic policy might deny the claim because you were working directly on that surface. A CCC rider typically adds an additional $150 to $300 to your annual pressure washing business insurance cost, but it is non-negotiable for professional contractors. Without it, you are essentially self-insuring the most common risk in the entire exterior cleaning industry.

Most specialized brokers, such as Joseph D. Walters or those affiliated with the Power Washers of North America (PWNA), include CCC as a standard feature of their trade-specific packages. These riders usually have a separate sub-limit, often ranging from $5,000 to $25,000 per occurrence, which covers the cost of repairing or replacing the client's property. If you accidentally use a 4000 PSI tip on delicate vinyl siding and cause $8,000 in damage, this rider is what prevents that mistake from bankrupting your small business. The peace of mind provided by this specific coverage far outweighs the marginal increase in your monthly premium payments.

When reviewing your policy documents, look for language specifically addressing 'property damage to your work' and 'property damage to your product.' Many generic insurance agents do not understand the nuances of soft washing versus high-pressure cleaning and may sell you a policy that is functionally useless for roof cleaning. Ensure your agent documents that you use sodium hypochlorite and other common surfactants, as some carriers have strict exclusions for chemical-related damage. Spending an extra $20 a month for a comprehensive rider is a smart investment that protects your long-term reputation and financial stability.

$1,100

Average Annual GL Premium

Based on a $1M/$2M policy for a solo operator with $100k revenue.

Key Takeaway: Always verify that your general liability policy includes a Care, Custody, and Control (CCC) rider to cover damage to the surfaces you are cleaning.

pressure washing business insurance cost: what you need and what it costs guide

Workers' Compensation Requirements and Pricing

Workers' compensation insurance is required by law in almost every state as soon as you hire your first employee, even if they are part-time or seasonal. In 2026, the cost is calculated based on your total payroll and the NCCI classification code assigned to pressure washing, which is often 0042 (Landscaping) or 9014 (Janitorial). For every $100 in payroll, you can expect to pay between $5 and $12 in premiums, depending on your state's specific rates and your company's safety record. This means a technician earning $40,000 per year could cost you an additional $2,000 to $4,800 annually in insurance overhead alone.

Many solo operators choose to exclude themselves from workers' comp coverage to save money, but this can be a risky move if you don't have a robust private disability policy. If you are injured on a job site and cannot work for three months, workers' comp provides wage replacement and covers 100% of your medical bills. Commercial property managers often require a workers' comp certificate even for solo owners to ensure they won't be held liable for injuries occurring on their premises. If you plan to bid on government contracts or large HOAs, having this coverage is a mandatory prerequisite for a successful bid.

To manage these costs, many contractors use a 'pay-as-you-go' workers' comp model, which links your premium payments directly to your actual payroll each month. This prevents the dreaded 'audit surprise' at the end of the year where you might owe thousands of dollars if your revenue exceeded your initial estimates. Using a platform like Hulo can help you track labor hours and payroll data accurately, making it much easier to report figures to your insurance carrier. Maintaining a safe work environment and documenting your safety training can also help lower your 'experience modifier' (E-Mod) score over time, eventually reducing your premiums.

Commercial Auto Insurance for Rigs and Trucks

Your personal auto insurance policy will almost certainly exclude coverage if you are involved in an accident while hauling a pressure washing trailer or transport chemicals for business use. Commercial auto insurance for a dedicated work truck typically costs between $1,200 and $2,400 per year, depending on the vehicle's weight and your driving history. If you have a custom-built flatbed rig with a 500-gallon water tank, the added weight increases the risk profile, which insurance companies reflect in higher premiums. A clean driving record is the most significant factor in keeping these costs toward the lower end of the spectrum.

In 2026, many carriers are requiring higher liability limits for commercial vehicles, often pushing for $500,000 or $1,000,000 in combined single limits (CSL). This is because the damage caused by a heavy truck and trailer in a multi-car pileup can easily exceed the standard $100,000 limits found on personal policies. You should also ensure that your policy includes 'Hired and Non-Owned Auto' coverage if you ever have employees driving their own vehicles for company errands. This specific add-on usually costs less than $150 per year but provides a critical layer of protection for the business entity.

The value of the equipment permanently attached to your truck should be specifically scheduled on your policy to ensure full replacement value in the event of a total loss. If you have a $15,000 hot water skid and a $3,000 custom hose reel system, don't assume the base auto policy covers them; they are often treated as 'cargo' or 'inland marine' items. Reviewing your policy annually is necessary as you upgrade your fleet or add more expensive cleaning technology to your rigs. Proper documentation, including photos and receipts of your build, will significantly speed up the claims process if an accident occurs.

Pro Tip: Use pay-as-you-go workers' comp to avoid large year-end audit bills and improve your monthly cash flow.

pressure washing business insurance cost: what you need and what it costs tips

Inland Marine Insurance for Mobile Equipment

Inland marine insurance, often called 'tools and equipment' coverage, protects your pressure washers, surface cleaners, and hoses while they are in transit or at a job site. For a typical equipment setup valued at $10,000, this coverage usually costs about $250 to $500 per year with a $500 deductible. Standard general liability does not cover the theft of your equipment from your trailer, which is a major risk in the exterior cleaning industry. Given that a single high-end surface cleaner costs $800, having this protection is essential for any contractor who stores equipment in a vehicle or trailer.

When selecting an inland marine policy, ensure it covers 'replacement cost' rather than 'actual cash value' (ACV). Actual cash value accounts for depreciation, meaning an insurance company might only pay you $2,000 for a five-year-old rig that costs $6,000 to replace today. Replacement cost coverage ensures you can get back to work immediately with new equipment without a massive out-of-pocket expense. You should maintain an updated inventory list with serial numbers and photos stored in the cloud to facilitate a smooth claims process. This documentation is also helpful for tax purposes and when valuing your business for a future sale.

Theft is the most common claim for inland marine policies in the pressure washing trade, especially for contractors working in urban areas. Many policies require that the equipment be stored in a locked vehicle or secured with specific anti-theft devices to remain valid. If you leave an unsecured pressure washer in the back of an open pickup truck overnight and it gets stolen, your claim could be denied based on 'failure to protect' clauses. Investing in high-quality trailer locks and GPS trackers for your most expensive skids can sometimes lead to premium discounts from savvy insurers.

Pollution and Environmental Liability

Environmental liability insurance is becoming increasingly important as local municipalities tighten regulations on wastewater runoff and chemical usage. A basic pollution occurrence rider can add $300 to $700 to your pressure washing business insurance cost, covering the cleanup of hazardous chemicals if a tank leaks into a storm drain. The EPA and local water authorities can levy fines exceeding $10,000 for a single violation of the Clean Water Act, making this coverage a vital safety net. Commercial clients, particularly industrial sites and gas stations, will often require proof of pollution coverage before awarding a contract.

This insurance covers not only the fines but also the professional remediation costs required to clean up a spill and the legal fees associated with environmental lawsuits. If a bleach spill kills a neighbor's expensive landscaping or contaminates a local pond, your standard liability policy will likely exclude the claim under the 'absolute pollution exclusion.' By adding a specific environmental endorsement, you protect your business from the catastrophic costs of accidental chemical discharge. It also demonstrates a level of professionalism and environmental stewardship that can help you win high-end residential and commercial bids.

Training your employees on spill containment and recovery is a prerequisite for many environmental policies and can help lower your risk profile. You should keep a spill kit on every truck, including absorbent booms and neutralizers, and document that your team knows how to use them. Insurance carriers view these proactive measures favorably and may offer lower rates to contractors who are certified by organizations like the UAMCC in environmental wash water recovery. As environmental regulations continue to evolve through 2026, having this coverage will separate the professional contractors from the 'splash and dash' operators.

| Coverage Type | Estimated Annual Cost | Recommended Limit |

|---|---|---|

| General Liability | $850 - $1,500 | $1M / $2M |

| Workers' Compensation | 5% - 12% of payroll | Statutory Limits |

| Commercial Auto | $1,200 - $2,500 | $500k - $1M CSL |

| Inland Marine | $250 - $600 | $10k - $25k Equipment Value |

| Pollution Liability | $300 - $800 | $50k - $100k Sub-limit |

2026 Estimated Annual Insurance Costs by Coverage Type

Key Takeaway: Inland marine insurance is the only way to protect your expensive pressure washing rigs from theft while they are on the road or at a job site.

pressure washing business insurance cost: what you need and what it costs for beginners

Starting Small: The Minimum Viable Insurance Package

For beginners just starting a pressure washing side hustle, the absolute minimum insurance package should include a general liability policy with a $1 million limit. You can often find introductory 'starter' policies for as low as $500 to $700 per year if you are only doing residential work and have no employees. However, be cautious of extremely cheap policies that have high deductibles or exclude critical services like roof cleaning or deck staining. Even as a beginner, a single mistake like using too much pressure on an old roof can result in a $15,000 damage claim that you cannot afford to pay out of pocket.

Using a modern business management tool like Hulo can help beginners manage these early overhead costs by consolidating their invoicing, scheduling, and customer communication into one affordable platform. By keeping your administrative costs low, you can afford to invest in better insurance coverage that protects your business as it grows. Many insurance companies will also give you a small discount if you can show that you have a professional system for documenting jobs and managing customer contracts. Professionalism from day one not only helps with insurance but also allows you to charge the premium rates necessary to cover your business expenses.

Avoid the temptation to operate without insurance 'just until you get a few jobs under your belt,' as this is the most dangerous time for your business. Most accidents happen during the learning phase when you are still mastering the equipment and chemical ratios. If you are caught working without insurance, you could face permanent bans from local lead generation platforms and be held personally liable for any damages. Think of your insurance premium as a mandatory startup cost, just like your pressure washer and chemicals, and factor it directly into your initial service pricing.

How to Get Your First Insurance Quote

To get an accurate insurance quote, you will need to provide your estimated annual revenue, the types of surfaces you will be cleaning, and the percentage of residential versus commercial work. Be honest about your experience level; while a lack of experience might slightly increase your initial premium, lying on an application can lead to a denied claim later. Many beginners find success using digital-first agencies like Thimble or Next Insurance, which offer monthly payment plans and instant COIs via a mobile app. This flexibility is perfect for new businesses that need to manage cash flow carefully during their first year of operation.

Once you receive a quote, take the time to read the 'Exclusions' section of the policy carefully to ensure you aren't paying for coverage that doesn't actually protect your work. Look for keywords like 'height restrictions'—some policies won't cover you if you work above two stories, which would make gutter cleaning or multi-story siding jobs uninsured. If you plan on doing any pressure washing from a ladder or a lift, you must ensure your agent is aware so they can place you with the correct carrier. A policy that is $200 cheaper but excludes 50% of your potential jobs is a poor investment.

Compare at least three different quotes from different brokers to ensure you are getting a competitive rate for your specific region. Specialized trade brokers often have access to 'programs' that generic local agents don't, which can result in better coverage for a lower price. Ask about 'bundle' discounts if you are also getting commercial auto or equipment coverage from the same provider. By the time you finish your first season, you will have a better understanding of your actual risks and can adjust your coverage limits accordingly for the next year.

$50 - $75

Starter Monthly Premium

Typical cost for a basic residential-only GL policy for new owners.

Ready to put this into action?

Hulo gives you everything to run your pressure washing business — website, CRM, scheduling, and invoicing. Join the waitlist for V2.

Join the Waitlistpressure washing business insurance cost: what you need and what it costs 2026

The Impact of Inflation and Tech on 2026 Rates

As we move through 2026, insurance premiums for trade contractors have stabilized but remain 10-15% higher than they were three years ago due to increased repair and medical costs. The price of high-end siding materials and custom automotive paint has risen, meaning insurance companies have to pay out more for the same 'minor' damage claims. To combat this, many insurers are now offering 'telematics' discounts for commercial auto policies, where you can save 10% by allowing the carrier to track your driving habits. This technology-driven approach is becoming the standard for contractors looking to keep their overhead manageable.

Another trend for 2026 is the rise of 'Cyber Liability' as a necessary add-on for pressure washing businesses that store customer credit card data and personal information. While it might seem unnecessary for a cleaning business, a data breach can cost a small company an average of $30,000 in notification fees and legal costs. Many insurance packages now include a small $50,000 cyber limit for an extra $100 per year, providing a safety net for your digital assets. As you move your business operations into the cloud, ensuring your digital footprint is as protected as your physical equipment is a mark of a mature company.

Climate change is also influencing pressure washing insurance, with some carriers increasing premiums in areas prone to severe drought or frequent hurricanes. In drought-stricken regions, the risk of accidental fires from hot-water pressure washers or chemical reactions is higher, leading to stricter underwriting requirements. Conversely, in hurricane-prone areas, the demand for post-storm cleanup is high, but so is the risk of injury on unstable job sites. Staying informed about how local environmental factors affect your specific market is crucial for accurate long-term financial planning and budgeting for your insurance needs.

The Role of Professional Certifications in Insurance

Professional certifications from organizations like the PWNA or UAMCC are becoming more influential in determining your pressure washing business insurance cost. Carriers are beginning to offer 'safety credits' to contractors who can prove they have completed formal training in ladder safety, chemical handling, and wastewater management. These credits can reduce your general liability premium by 5% to 10%, effectively paying for the cost of the certification within the first year. Beyond the financial savings, being a certified professional allows you to market yourself as a lower-risk option to high-value commercial clients.

In 2026, many insurance companies are also looking for contractors who use specialized software to document their safety protocols and job site conditions. By using Hulo to take 'before and after' photos and having customers sign digital waivers that acknowledge existing damage, you create a paper trail that can quickly dismiss frivolous claims. Insurance adjusters love this level of documentation, as it makes their jobs easier and reduces the likelihood of a payout for pre-existing conditions. Proactive risk management through technology is one of the most effective ways to negotiate better rates with your insurance underwriter.

Continuing education is no longer just for high-end specialized trades; it is a vital part of running a modern pressure washing business. Attending industry trade shows and staying updated on the latest soft-washing techniques can prevent the type of damage that leads to massive premium hikes. A single claim can stay on your record for three to five years, potentially doubling your insurance costs over that period. Investing time in training and certification is a proactive strategy that keeps your loss history clean and your insurance premiums at the most competitive levels possible.

Key Takeaway: In 2026, technology like telematics and job-site documentation software is the best way to secure discounts on your insurance premiums.

How Can You Lower Your Insurance Costs Without Sacrificing Coverage?

Increasing Deductibles and Bundling Policies

One of the fastest ways to lower your monthly pressure washing business insurance cost is to increase your per-claim deductible. Moving from a $500 deductible to a $2,500 deductible can often reduce your annual premium by 15% to 25%. However, you must ensure that you have this deductible amount sitting in a dedicated business emergency fund so that a single claim doesn't cause a cash flow crisis. This strategy effectively makes you 'self-insured' for minor incidents while keeping the big-ticket protection for catastrophic events that could actually end your business.

Bundling your various policies—General Liability, Commercial Auto, and Inland Marine—with a single carrier is another effective way to secure a 'multi-policy' discount. Most major insurers offer a 5% to 10% reduction when you give them all of your business, and it also simplifies your administration by having a single renewal date and point of contact. Furthermore, some carriers offer 'Package Policies' specifically designed for mobile contractors that combine these coverages at a lower price point than buying them individually. Always ask your broker if there are any available bundles or trade-specific packages that you might have missed.

Review your policy limits annually to ensure you aren't paying for more coverage than you actually need as your business fluctuates. If you sold off a trailer or downsized your crew, make sure those changes are reflected in your policy immediately to stop paying unnecessary premiums. Conversely, if you have significantly increased your revenue, don't wait for an audit to update your limits, as this can lead to penalties and coverage gaps. Staying proactive with your insurance agent ensures that your coverage is always 'right-sized' for your current operational reality, preventing both overpayment and under-insurance.

Implementing a Formal Safety Program

Insurance companies are in the business of predicting risk, and nothing says 'low risk' like a contractor with a documented safety program. Create a simple safety manual that outlines your procedures for ladder usage, chemical mixing, and job site setup, and have every employee sign it during onboarding. Provide regular 'tailgate safety meetings' and document the topics covered and the attendance to show your insurer that safety is part of your daily culture. Many carriers will offer a 5% 'safety credit' just for having these documented processes in place, as it statistically reduces the frequency of claims.

Investing in high-quality equipment with built-in safety features can also help you negotiate lower rates with certain specialized underwriters. For example, using remote-controlled hose reels and soft-wash systems that allow technicians to stay on the ground reduces the risk of ladder falls, which are the most expensive type of workers' comp claims. When you buy new equipment, tell your insurance agent about the safety benefits and ask if it qualifies you for a different risk classification. Modern equipment is often safer and more efficient, providing a double benefit of lower insurance costs and higher productivity on the job.

Finally, use your business software to track and report on your safety milestones, such as '500 days without a lost-time accident.' Sharing these statistics with your insurance broker during the renewal process gives them the ammunition they need to fight for a lower rate from the underwriters. It proves that your business is managed by data and professional standards rather than luck and guesswork. In the competitive 2026 market, these small percentage gains in overhead reduction can be the difference between a struggling business and a highly profitable one.

Pro Tip: Set aside your deductible amount in a high-yield savings account so you can confidently opt for higher-deductible, lower-premium policies.

Wrapping Up

Securing the right insurance is a fundamental step in building a sustainable and profitable pressure washing business. By understanding the specific costs associated with general liability, workers' comp, and specialized riders like CCC, you can protect your assets and win higher-value contracts. Use the benchmarks in this guide to audit your current coverage and ensure your business is fully protected for the 2026 season.

Frequently Asked Questions

How much does pressure washing business insurance cost on average?

In 2026, a typical solo pressure washing contractor can expect to pay between $850 and $2,500 annually for a comprehensive insurance package. This range includes general liability, a basic inland marine policy for equipment, and a commercial auto policy for one truck. Costs vary significantly based on your state, total revenue, and whether you offer high-risk services like roof cleaning.

What's the difference between General Liability and Care, Custody, and Control (CCC)?

General Liability covers damage to third-party property, such as accidentally hitting a neighbor's car with your pressure stream, while CCC covers the specific item you are being paid to clean. Without a CCC rider, your insurance may deny a claim if you damage the deck or siding you were hired to wash. Professional pressure washers should always ensure their policy includes a CCC endorsement to avoid massive out-of-pocket repair costs.

Do I need a license to get pressure washing insurance?

While many insurance companies will issue a policy without a state-level trade license, having one often leads to lower premiums and better coverage options. In states where pressure washing is a regulated trade, such as California or parts of Florida, you must provide your license number to secure a professional-grade policy. Operating without a required license can also be grounds for an insurance company to deny a claim if an accident occurs.

How long does it take to get a Certificate of Insurance (COI)?

With modern digital insurance providers like Next or Thimble, you can receive a COI via email within minutes of completing your application and making a payment. Traditional brokers may take 24 to 48 hours to process your request and issue the document. It is best to have your COI ready before you start bidding on commercial jobs, as property managers often require it as part of the initial vendor packet.

What certifications do I need for Pressure Washing in 2026?

While not always legally required, certifications from the PWNA (Power Washers of North America) or UAMCC (United Association of Mobile Contract Cleaners) are highly recommended. These certifications prove to both customers and insurance companies that you have mastered safe cleaning techniques and environmental compliance. Many insurance carriers offer premium discounts to contractors who hold these specific industry credentials.

How do I get paid faster as a Pressure Washing contractor?

Using an integrated platform like Hulo allows you to send digital invoices immediately upon job completion and accept credit card payments on the spot. By automating your follow-ups and offering easy payment links, you can reduce your average collection time from 15 days to less than 48 hours. Faster payments improve your cash flow, making it easier to stay current on your insurance premiums and other business overhead.

Is a hot water pressure rig more expensive to insure?

Yes, hot water rigs typically carry higher insurance premiums because they introduce a fire risk and the potential for severe thermal burns. Insurance companies view the pressurized heating coils and fuel tanks as additional hazards compared to cold water units. You can expect to pay an additional $100 to $300 per year on your inland marine and liability policies to account for the increased risk profile of a hot water system.

Does insurance cover damage to a customer's plants or landscaping?

Standard general liability might cover landscaping damage, but many policies have 'pollution exclusions' that could lead to a denial if the damage was caused by chemical runoff like bleach. To ensure you are covered for dead grass or ruined flowers, you need a pollution liability rider or a specific 'pesticide/herbicide' endorsement. This is especially critical for soft-washing businesses that use high concentrations of sodium hypochlorite.

Should I buy 'per-project' insurance or an annual policy?

Per-project insurance is useful for very occasional side hustles, but if you are doing more than one job a month, an annual policy is almost always more cost-effective. Annual policies provide continuous coverage, which is necessary to maintain your reputation and meet the requirements of most commercial clients and lead-generation sites. Furthermore, annual policies allow you to build a 'tenure' with a carrier, which leads to lower rates and better loyalty discounts over time.

Stop Overpaying for Pressure Washing Overhead

Hulo combines your website, CRM, invoicing, and scheduling into one powerful tool for under $50/mo. Start your free trial today and keep more of your hard-earned profit.

Join the WaitlistMore from the Blog

9 Expert Tips for the Best Pressure Washer for Starting a Business (2026)

The best pressure washer for starting a business is a gas-powered unit delivering at least 4.0 GPM (gallons per minute) ...

9 Actionable Ways to Bid Commercial Pressure Washing Jobs for Contractors (2026)

Bidding commercial pressure washing jobs requires calculating your square footage rate, typically between $0.10 and $0.5...

How to Price Pressure Washing Jobs: Complete Pricing Guide (2026)

In 2026, the exterior cleaning industry has moved far beyond the 'guy with a truck' mentality, evolving into a data-driv...