10 Smart Roofing Business Insurance Requirements for Contractors (2026)

15 min read·Updated April 4, 2026Roofing business insurance requirements typically mandate a minimum of $1 million in general liability coverage, statutory workers' compensation for all employees, and commercial auto insurance for company vehicles. Most states also require roofing contractors to hold a surety bond ranging from $10,000 to $25,000 to maintain active licensing with state boards like the NRCA. Operating without these coverages exposes your business to catastrophic financial loss from OSHA fines, which can exceed $15,000 per violation, or personal injury lawsuits that average over $100,000 in the roofing sector. In this guide, you will learn the exact policy limits, specific endorsements, and current 2026 pricing benchmarks required to keep your roofing business compliant and protected.

Table of Contents

Step-by-Step Overview

- 1

Secure General Liability Insurance

Obtain a General Liability (GL) policy with a minimum limit of $1,000,000 per occurrence and $2,000,000 aggregate. This covers third-party bodily injury and property damage, which are high-risk areas for roofers. Expect to pay between $2,500 and $6,000 annually depending on your gross revenue and claims history. Ensure the policy specifically includes 'completed operations' coverage to protect against leaks that occur months after the job is finished.

- 2

Establish Workers' Compensation Coverage

Set up Workers' Comp through your state fund or a private carrier like Travelers or Liberty Mutual. In roofing, rates are high—often $15 to $30 for every $100 of payroll—due to the risk of falls. This insurance is legally required in 49 states for any business with employees. Proper coverage prevents the business from being directly sued for workplace injuries and covers medical expenses and lost wages for injured crew members.

- 3

Purchase Commercial Auto Insurance

Insure all company trucks and vans under a commercial policy with at least $500,000 in combined single limits (CSL). Personal auto policies will not cover accidents that occur while hauling shingles or towing a dump trailer. Annual premiums for a single roofing truck typically range from $1,800 to $3,200. This coverage is essential for protecting your fleet and satisfying the requirements of commercial clients who demand proof of auto insurance.

- 4

Add Inland Marine (Tool & Equipment) Coverage

Protect your ladders, nail guns, and generators with an Inland Marine floater. Standard GL policies do not cover your own equipment if it is stolen from a job site or damaged in transit. For $10,000 worth of roofing equipment, expect to pay approximately $250 to $500 per year. This is a critical requirement for businesses that store expensive materials like copper or specialized slate-cutting tools on-site.

- 5

Obtain a State-Required Surety Bond

Apply for a contractor license bond through a surety company to satisfy state licensing board requirements. These bonds usually range from $10,000 to $25,000 and cost between 1% and 3% of the bond amount annually if you have good credit. The bond serves as a financial guarantee to the state and your customers that you will follow local building codes and fulfill your contractual obligations.

- 6

Implement an Umbrella or Excess Liability Policy

Layer an additional $1 million to $5 million of coverage over your primary GL and Auto policies. Many commercial general contractors (GCs) require roofers to have at least $5 million in total liability to step foot on a commercial job site. An umbrella policy is relatively affordable, often costing $500 to $1,500 per year for the first million in extra protection, providing a necessary safety net for high-value projects.

How to roofing business insurance requirements: what coverage you need?

General Liability for Roofing Hazards

General liability (GL) insurance is the foundation of any roofing business insurance requirements strategy, providing protection against third-party claims. For roofing contractors, this primarily covers bodily injury, such as a homeowner tripping over a ladder, and property damage, like a heavy bundle of shingles falling through a skylight. Most industry experts recommend a minimum limit of $1,000,000 per occurrence, as even minor roofing accidents can quickly escalate into six-figure legal settlements.

Beyond basic damage, your GL policy must include 'Products and Completed Operations' coverage. This specific endorsement protects your business if a roof you installed two years ago suddenly fails and causes $50,000 in water damage to the home's interior. Without this, your liability ends the moment you leave the job site, leaving you personally responsible for any future warranty-related structural damage or mold claims that may arise.

When selecting a GL policy, pay close attention to the 'Open Roof' exclusion, which is common in cheaper roofing policies. An open roof exclusion means the insurance company will not pay for rain damage if you leave a roof uncovered overnight during a project. To remain fully protected, you must ensure your policy specifically covers 'open roof' scenarios, even if it increases your annual premium by 15% to 20%, as one unexpected storm can bankrupt an uninsured company.

The Role of Professional Liability in Roofing

While GL covers physical damage, Professional Liability—also known as Errors and Omissions (E&O)—covers financial loss resulting from your advice or design work. If you recommend a specific type of TPO membrane for a flat commercial roof that turns out to be incompatible with the existing structure, the resulting repair costs could fall under E&O. In 2026, many commercial clients require roofing firms to carry at least $500,000 in E&O coverage to mitigate design-related risks.

Professional liability is particularly important for roofing contractors who offer consulting services or custom drainage designs. For example, if your drainage calculations are off and cause water to pool, leading to a structural collapse, a standard GL policy might deny the claim because the damage resulted from a design error rather than an accident. E&O policies for small roofing firms typically cost between $800 and $1,500 annually but are indispensable for high-end residential and commercial work.

Integrating your insurance management with a platform like Hulo can help you track these policy renewals and certificate requests effortlessly. Hulo allows you to store digital copies of your COIs and set automated reminders 30 days before a policy expires, ensuring you never face a gap in coverage. This level of organization is often a prerequisite for working with large property management firms that demand constant proof of active, high-limit professional liability insurance.

$1,000,000

Minimum Recommended GL Limit

Standard requirement for 90% of residential roofing contracts in 2026.

Key Takeaway: Always verify that your General Liability policy includes 'Completed Operations' and lacks an 'Open Roof' exclusion to avoid catastrophic out-of-pocket expenses.

Roofing business insurance requirements: what coverage you need guide to Workers' Comp?

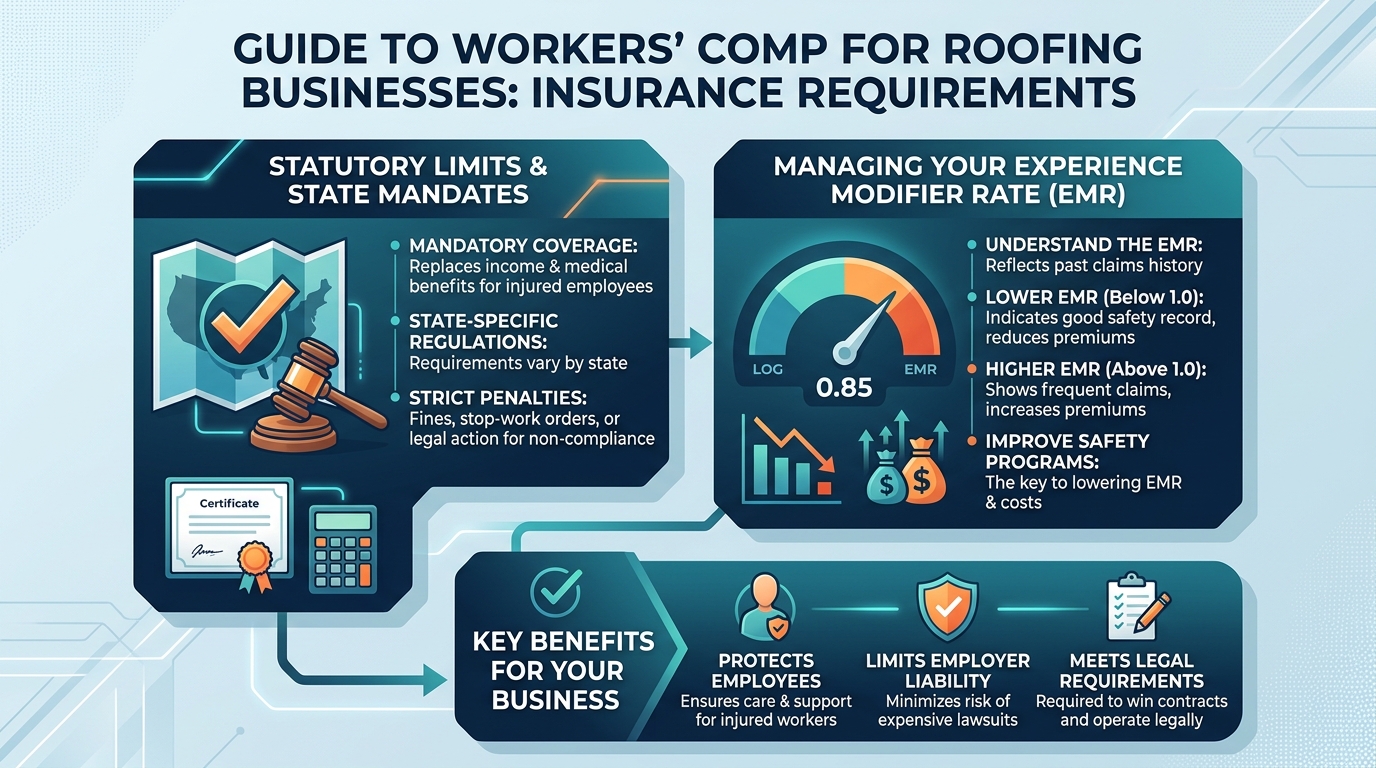

Statutory Limits and State Mandates

Workers' compensation is a non-negotiable component of roofing business insurance requirements in nearly every US state. Because roofing is classified as a high-hazard trade by the NCCI (National Council on Compensation Insurance), your premiums will be significantly higher than those for painters or electricians. In states like Florida or California, roofing workers' comp rates can exceed 25% of your total payroll costs, meaning for every $40,000 you pay a lead installer, you may owe $10,000 in insurance premiums.

This coverage pays for medical bills, rehabilitation, and a portion of lost wages if a crew member falls from a roof or suffers heatstroke on a 100-degree day. In 2026, OSHA's focus on fall protection has intensified, and having a valid workers' comp policy is often the first thing an inspector will verify during a site visit. If an employee is injured and you do not have coverage, the state can seize your business assets and personal property to cover the medical costs, which often exceed $250,000 for a serious fall.

Even if you are a sole proprietor with no employees, many general contractors will require you to carry a 'ghost policy' or a minimum workers' comp policy to step onto their job sites. This ensures that if you are injured, the GC's own insurance policy isn't triggered, which would spike their EMR rating. A ghost policy typically costs between $750 and $1,200 per year and provides a Certificate of Insurance (COI) without offering actual medical benefits to the owner.

Managing Your Experience Modifier Rate (EMR)

Your Experience Modifier Rate, or EMR, is a multiplier applied to your workers' comp premiums based on your safety record over the last three years. A standard EMR is 1.0; if your safety record is excellent, your EMR might drop to 0.85, giving you a 15% discount on your insurance. Conversely, if you have frequent claims, your EMR could jump to 1.5, effectively increasing your $20,000 premium to $30,000 and making your bids less competitive against safer companies.

To keep your EMR low, you must implement a rigorous safety program that includes weekly 'Toolbox Talks' and mandatory use of OSHA-compliant fall arrest systems. Many modern insurance carriers offer premium credits if you can prove you use digital safety tracking tools or provide regular NATE-style training for your crew. Documenting these safety sessions is vital, as it provides evidence to your insurance auditor that you are actively mitigating high-altitude risks.

By using a business management tool like Hulo, you can store safety logs and incident reports in one central location, which simplifies the annual insurance audit process. When the auditor sees organized records of safety training and equipment inspections, they are more likely to view your business as a 'preferred risk.' This proactive approach to risk management can save a roofing company with a $100,000 payroll upwards of $5,000 annually in avoided premium surcharges.

Pro Tip: Check your EMR annually; a score above 1.0 can disqualify you from bidding on most government and large-scale commercial roofing projects.

Roofing business insurance requirements: what coverage you need tips for inland marine?

Protecting Tools in Transit and On-Site

Inland Marine insurance is a specialized coverage that protects your roofing tools and materials while they are away from your primary warehouse. Standard commercial property insurance usually only covers items within 1,000 feet of your office, which is useless for a roofing crew working 20 miles away. An Inland Marine policy covers your nailers, compressors, and expensive tear-off machines against theft, fire, and damage during transport in your trucks.

Theft is a massive issue in the roofing industry, with job site equipment losses increasing by 12% annually according to recent 2026 crime statistics. If a thief breaks into your trailer and steals $8,000 worth of cordless tools, an Inland Marine policy with a $500 deductible will cover the replacement cost. Without it, you would have to pay the full $8,000 out of pocket, which could wipe out the entire profit margin of a residential roof replacement job.

When setting up your policy, ensure you have 'Installation Floater' coverage included, which protects uninstalled materials like shingles or metal panels sitting on a pallet at the job site. If a storm ruins $15,000 worth of materials before they are attached to the roof, the installation floater pays for the replacement. This is a critical requirement for large projects where you might have $50,000+ in materials staged on-site for several weeks.

Coverage for Rented and Leased Equipment

Many roofing contractors rent specialized equipment like telehandlers, cranes, or 40-foot boom lifts for steep-slope or commercial projects. Rental yards like United Rentals or Sunbelt usually require proof of 'Rented Equipment' coverage before they will release the machine to you. Adding this to your Inland Marine policy is significantly cheaper than buying the 'damage waiver' offered by the rental company, which can cost $50 to $100 per day.

A typical 'Rented Equipment' endorsement provides up to $100,000 in coverage for a flat annual fee of around $300 to $600. This covers accidental damage to the machine, such as a boom lift tipping over or a hydraulic line bursting while in your care. Given that a new telehandler can cost over $120,000, this small addition to your roofing business insurance requirements is a high-value investment that protects your liquid capital.

It is also wise to verify if your policy includes 'Lease Gap' coverage if you are financing your vehicles or heavy machinery. If a truck is totaled and you owe more than its current market value, gap insurance covers the difference so you aren't stuck paying for a vehicle you can no longer use. This is especially relevant in 2026, as the rapid depreciation of specialized roofing trucks can leave a significant financial hole after an accident.

$250 - $500

Avg. Annual Inland Marine Cost

Covers approximately $10,000 in tools and equipment.

Roofing business insurance requirements: what coverage you need for beginners: Surety Bonds?

Understanding the License Bond

For beginners, the difference between insurance and a surety bond is often confusing, yet both are core roofing business insurance requirements. While insurance protects your business from losses, a surety bond protects the consumer and the state from your business's failure to perform. If you take a $5,000 deposit for a roof and never show up, the homeowner can file a claim against your license bond to recover their money.

In states like Arizona or California, you cannot even obtain a contractor's license without a valid bond on file with the registrar. These bonds are relatively inexpensive for contractors with decent credit, often costing $150 to $400 per year for a $15,000 bond. However, if your credit score is below 600, you might be forced into a 'high-risk' pool where the same bond could cost $1,500 or more annually, making it a significant barrier to entry.

It is crucial to understand that a bond is not 'free money' for you; if a claim is paid out by the surety company, you are legally obligated to pay them back every cent. A single bond claim can lead to the immediate suspension of your roofing license, effectively shutting down your business until the debt is settled. Therefore, maintaining high quality standards and clear communication with clients is the best way to protect your bond and your professional reputation.

Bid, Performance, and Payment Bonds

As you grow from small residential repairs to larger commercial or municipal contracts, you will encounter bid and performance bonds. A bid bond guarantees that if you win a contract, you will actually sign it and provide the required performance bonds. Performance bonds, meanwhile, guarantee that you will complete the project according to the specifications and within the agreed timeframe, providing peace of mind to the building owner.

Payment bonds are often paired with performance bonds and ensure that you will pay all your subcontractors and material suppliers. In the roofing world, where a single job might require $100,000 in shingles from a supplier like ABC Supply, a payment bond protects the property owner from having a mechanic's lien placed on their building if you fail to pay the bill. These bonds usually cost 1% to 3% of the total contract value and are often factored into the project's bid price.

Using a tool like Hulo to manage your project workflows ensures you have the documentation needed to secure these larger bonds. Surety companies will ask for your financial statements, work-in-progress (WIP) reports, and proof of past successful projects before issuing a $500,000 performance bond. Having your project data organized in a CRM makes this underwriting process much faster, allowing you to bid on lucrative government roofing contracts that competitors might miss.

Key Takeaway: A license bond is a legal requirement for your roofing license, but performance bonds are the key to unlocking high-value commercial contracts.

Ready to put this into action?

Hulo gives you everything to run your roofing business — website, CRM, scheduling, and invoicing. Join the waitlist for V2.

Join the WaitlistRoofing business insurance requirements: what coverage you need 2026: Cyber and Pollution?

Cyber Liability for Digital Roofing Businesses

By 2026, even small roofing companies are highly digitized, using cloud-based software to store customer addresses, credit card info, and roof photos. This makes you a target for ransomware and data breaches, which can cost a small business an average of $35,000 to remediate. Cyber liability insurance covers the cost of notifying customers, forensic investigations, and even the lost income if your systems are locked down by hackers.

Many roofers mistakenly believe they are too small to be targeted, but automated bots don't care about your company size. If your email is hacked and a fraudster sends fake bank wiring instructions to a commercial client for a $50,000 roof payment, you could be held liable for the loss. A basic cyber policy for a roofing contractor typically costs $500 to $1,000 per year and provides a critical layer of protection for your digital assets.

Hulo helps mitigate this risk by providing a secure, encrypted platform for managing your business operations, but insurance remains a necessary backstop. When you combine secure software with a robust cyber policy, you significantly reduce the risk of a digital catastrophe. This is increasingly becoming a requirement for roofing contractors who work with large insurance carriers on storm restoration claims, as those carriers demand high levels of data security.

Pollution and Environmental Liability

Pollution liability is an often-overlooked aspect of roofing business insurance requirements, particularly for contractors involved in tear-offs or flat roofing. If you are removing an old roof and asbestos-containing materials are disturbed and released into the neighborhood, a standard GL policy will almost certainly exclude the resulting cleanup costs. Pollution insurance covers the expensive remediation and legal fees associated with environmental contamination.

For flat roofing contractors using torch-down methods or chemical adhesives, pollution coverage is even more vital. A leak from a chemical drum that seeps into a local storm drain can result in EPA fines exceeding $25,000 per day until the mess is cleared. In 2026, environmental regulations are stricter than ever, and many commercial property owners will not hire a roofing company that doesn't carry at least $1 million in pollution liability.

This coverage also applies to mold claims, which are a common headache in the roofing industry. If a roof leak occurs during a project and leads to a massive mold outbreak inside a client's home, pollution liability can cover the specialized mold remediation costs that standard GL policies often cap or exclude entirely. Adding a pollution endorsement to your existing package usually costs between $1,000 and $2,500 annually but can save your business from an environmental lawsuit.

Pro Tip: If you perform any work on buildings built before 1980, check your policy for asbestos exclusions and consider a standalone pollution policy.

How much does roofing business insurance cost in 2026?

Premium Breakdowns by Policy Type

The total cost of roofing business insurance requirements for a typical small company with 3-5 employees usually ranges from $12,000 to $25,000 per year. General Liability remains the largest chunk for many, averaging $3,500 to $7,000, while Workers' Comp can easily exceed $10,000 depending on your payroll. These costs are a significant overhead expense, but they are also tax-deductible business expenses that demonstrate your legitimacy to potential clients.

Commercial auto insurance for two roofing trucks will likely cost around $4,500 annually, assuming clean driving records for all crew members. If you have a driver with a recent DUI or multiple speeding tickets, your auto premiums could double or the carrier may refuse to cover that specific driver entirely. It is standard practice to run a Motor Vehicle Report (MVR) on every new hire before they are allowed to get behind the wheel of a company vehicle.

To manage these costs, many roofers opt for 'pay-as-you-go' workers' comp, which calculates your premium based on your actual monthly payroll rather than an estimate. This prevents a massive, unexpected audit bill at the end of the year and helps with cash flow management during the slower winter months. Platforms like Hulo integrate with payroll systems to make this reporting automatic, ensuring your insurance costs scale naturally with your business volume.

Factors That Influence Your Rates

Your geographic location is one of the biggest drivers of insurance costs; a roofing contractor in hail-prone Texas or hurricane-prone Florida will pay significantly more for GL than a contractor in a stable climate like Ohio. Furthermore, the type of roofing you do matters—residential asphalt shingle work is viewed as lower risk than commercial hot-mop or high-rise slate work. Insurance carriers use actuarial data to price these risks, and 'hot work' involving torches can increase premiums by 50% or more.

Your years in business also play a role; a new start-up will often pay a 'new venture' surcharge because they lack a proven safety track record. Once you have three to five years of continuous coverage without major claims, you become eligible for 'preferred' markets with lower rates and better coverage terms. This is why it is vital to avoid any lapses in coverage, as even a 30-day gap can reset your 'years in business' clock with many insurance carriers.

Finally, your chosen deductible level can help lower your annual premiums. Moving from a $500 deductible to a $2,500 deductible on your GL policy can save you 10-15% on your premium, but you must ensure you have that cash set aside in an emergency fund. In 2026, savvy roofers use the savings from higher deductibles to invest in better safety equipment, which eventually leads to a lower EMR and even greater long-term insurance savings.

| Policy Type | Estimated Annual Cost | Typical Limit |

|---|---|---|

| General Liability | $3,500 - $7,500 | $1M / $2M |

| Workers' Compensation | $8,000 - $15,000 | Statutory |

| Commercial Auto | $2,000 - $4,500 | $500k CSL |

| Inland Marine | $300 - $800 | $15k Coverage |

| Surety Bond | $150 - $500 | $15k Bond |

| Umbrella Policy | $600 - $1,500 | $1M Excess |

Estimated Annual Insurance Premiums for Roofing (2026)

Wrapping Up

Meeting all roofing business insurance requirements is a significant but necessary investment that separates professional contractors from fly-by-night operations. By securing high-limit general liability, statutory workers' comp, and specialized inland marine coverage, you protect your assets and gain the trust of high-value clients. Start by auditing your current policies today and implementing a digital management system to ensure you never miss a renewal or a bond payment.

Frequently Asked Questions

How much does roofing general liability insurance cost in 2026?

For a small roofing company with $500,000 in annual revenue, General Liability insurance typically costs between $3,500 and $6,000 per year. Factors like your state, your use of subcontractors, and whether you perform 'hot work' with torches can push these premiums higher. Most policies carry a $1,000 deductible per claim for property damage.

What's the difference between a roofing license bond and general liability insurance?

A license bond is a financial guarantee that protects the consumer and the state if you fail to follow building codes or finish a job, whereas general liability insurance protects your business from lawsuits involving bodily injury or property damage. If a bond claim is paid, you must reimburse the surety company, but an insurance claim is paid out by the carrier without you having to pay it back (other than your deductible).

Do I need workers' compensation if I only use 1099 subcontractors?

Yes, in most states, if a 1099 subcontractor does not have their own workers' comp insurance, the state considers them your employee in the event of an injury. If they fall and get hurt, you will be held liable for their medical bills, which can easily exceed $100,000. Always collect a Certificate of Insurance (COI) from every subcontractor to ensure they carry their own coverage.

How long does it take to get a Certificate of Insurance (COI) for a new job?

A standard COI can usually be issued by your insurance agent within 24 to 48 hours. However, if a commercial client requires specific 'additional insured' wording or a waiver of subrogation, it may take 3-5 business days for the carrier's underwriting department to approve the change. Using a digital platform like Hulo to store your insurance details can speed up the process of requesting these documents.

What certifications do I need to lower my roofing insurance premiums?

Earning certifications from the NRCA (National Roofing Contractors Association) or manufacturer-specific credentials from GAF or Owens Corning can often lead to 5-10% discounts on your GL or E&O premiums. These certifications demonstrate to insurers that your crew follows industry-standard installation and safety protocols, making you a lower-risk client. Additionally, maintaining a certified safety program can lower your EMR for workers' comp.

How do I get paid faster as a roofing contractor to cover insurance costs?

Using a professional invoicing and CRM tool like Hulo allows you to send digital invoices with credit card and ACH payment options, which typically results in getting paid 3-5 days faster than traditional paper checks. Faster cash flow ensures you have the liquidity to pay your monthly insurance premiums on time, avoiding late fees or policy cancellations. You can also automate follow-ups for unpaid invoices to keep your accounts receivable under control.

Is inland marine insurance worth it for a small roofing business?

Yes, inland marine insurance is highly worth it because it covers your tools—like nail guns, compressors, and ladders—wherever they go. A standard business property policy only covers items at your office, but most roofing theft occurs at the job site or from your truck. For as little as $300 a year, you can protect $10,000+ in equipment, which is a small price to pay for peace of mind.

What is an EMR rating and why does it matter for roofers?

The Experience Modifier Rate (EMR) is a number used by insurance companies to gauge your past cost of injuries and future risk. A 1.0 is the industry average; if your EMR is 1.2, you pay 20% more for workers' comp than the average roofer. Conversely, an EMR of 0.80 means you get a 20% discount, giving you a massive competitive advantage when bidding on large projects.

Does roofing insurance cover leaks after the job is finished?

Only if your policy includes 'Completed Operations' coverage. This specific part of a General Liability policy covers damage that occurs after you have handed the project over to the owner. Without it, you would be personally liable for water damage caused by a leak that appears six months after the installation is complete.

What is the 'Open Roof' exclusion in roofing insurance?

An 'Open Roof' exclusion is a clause in some cheap insurance policies that states the carrier will not pay for water damage if you leave a roof uncovered during a project and it rains. Because this is a common occurrence in roofing, you should always insist on a policy that removes this exclusion, even if it costs slightly more, to ensure you are protected against sudden weather changes.

Professionalize Your Roofing Business with Hulo

Hulo provides the all-in-one platform roofing contractors need to manage invoicing, track safety logs for insurance audits, and store digital COIs. Scale your business in 2026 while keeping your risk management organized and your overhead low.

Join the WaitlistMore from the Blog

7 Smart Steps to How to Estimate a Roofing Job for Contractors (2026 Guide)

To estimate a roofing job, you must calculate the total square footage of the roof and divide by 100 to determine the nu...

11 Expert Ways to Get Roofing Leads Without Door Knocking for Contractors (2026)

To get roofing leads without door knocking, you must implement a multi-channel digital strategy focusing on Google Local...

How to Get Roofing Leads: 15 Proven Strategies for 2026

The roofing industry in 2026 is a $56.7 billion market, yet many contractors struggle to maintain a consistent pipeline ...